Introduction to fixed assets

Fixed assets are tangible or physical assets that a company owns and uses for its business operations, with the expectation of deriving benefits from them over an extended period, typically exceeding one year. These assets are crucial in generating revenue and achieving its business objectives. Fixed assets are also referred to as non-current assets or long-term assets. In this blog, we are breaking down everything there’s to know about fixed assets – from what fixed assets, their importance, and their benefits. Keep reading to know more.

What are fixed assets?

Fixed assets, or non-current or long-term assets, are tangible or physical assets that a company owns and uses for its business operations. These assets are not meant for immediate sale or consumption but are intended for long-term use, typically exceeding one year. Fixed assets are crucial for a business’s smooth functioning and growth, as they provide the necessary infrastructure and tools to produce goods and services efficiently.

Importance of fixed assets

Fixed assets play a crucial role in the success and stability of a business, making them of utmost importance for several reasons:

- Long-term value creation: Fixed assets are essential for generating revenue and profits over an extended period. They serve as the foundation for a company’s operations, enabling it to produce goods and provide services efficiently and consistently.

- Asset base and financial health: Fixed assets constitute a significant portion of a company’s total assets, representing its long-term investments. The value of fixed assets reflected on the balance sheet showcases the company’s financial strength and capacity for growth.

- Credibility and creditworthiness: Companies with well-managed fixed assets often enjoy better credibility among stakeholders, including investors, lenders, and business partners. This, in turn, can lead to improved access to funding and favorable terms for loans or investments.

- Operational efficiency: Properly maintained fixed assets contribute to enhanced productivity and efficiency within the organization. Up-to-date equipment and machinery ensure smooth operations, reducing downtime and improving overall performance.

- Risk mitigation: Adequate fixed asset management involves maintenance and safety protocols, reducing the likelihood of accidents, breakdowns, or legal liabilities. This, in turn, minimizes potential financial risks for the business.

- Compliance and reporting: Accurate accounting and reporting of fixed assets are essential for meeting regulatory requirements and financial standards, ensuring transparency and reliability in financial statements.

- Strategic decision-making: Understanding the value and condition of fixed assets allows businesses to make informed decisions regarding upgrades, replacements, or expansions. It facilitates strategic planning and resource allocation.

Quick Read: Capital Investment: Meaning, Types, How it Works & Examples

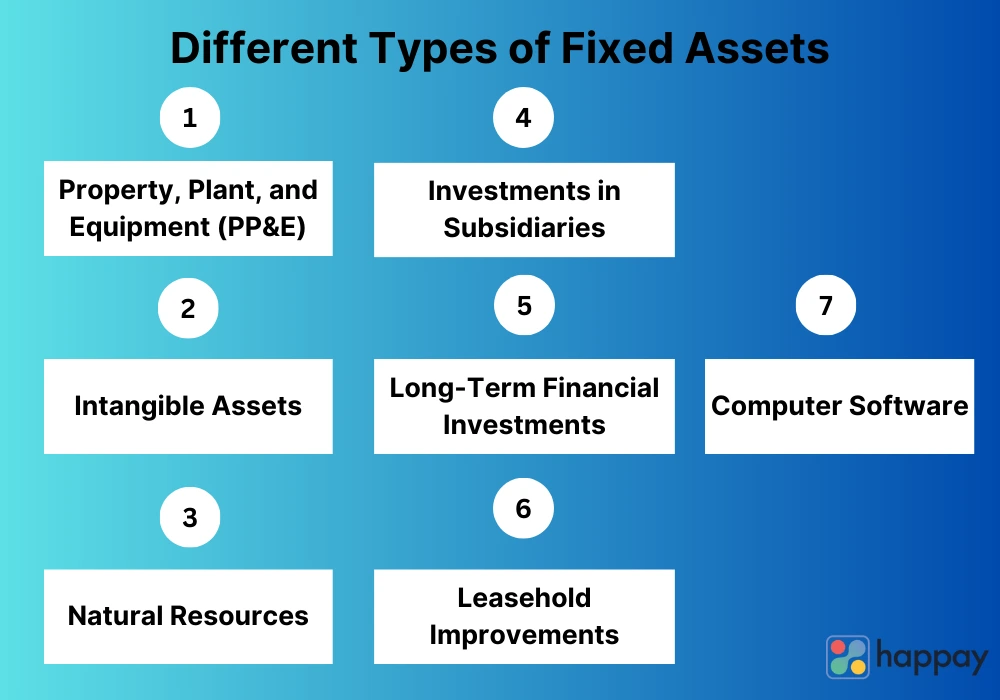

What are the different types of fixed assets?

Fixed assets can be categorized into various types based on their nature, usage, and characteristics. Some common types of fixed assets include:

- Property, Plant, and Equipment (PP&E): This category includes tangible assets used in the production and operation of the business. It comprises buildings, land, machinery, equipment, vehicles, and furniture.

- Intangible Assets: Unlike tangible assets, intangible assets have no physical presence but hold significant value for a company. Examples include patents (exclusive rights to an invention), trademarks (distinctive signs representing a brand), copyrights (protection for original creative works), and goodwill (the value of a company’s reputation and customer base).

- Natural Resources: Fixed assets that come from nature and have economic value are classified as natural resources. Examples include oil reserves, mineral deposits, timberland, and water rights.

- Investments in Subsidiaries: Companies may own many other businesses (subsidiaries) as part of their long-term investment strategy. These ownership stakes are considered fixed assets.

- Long-Term Financial Investments: These fixed assets represent investments in financial instruments that the company intends to hold for an extended period, such as long-term bonds or other securities.

- Leasehold Improvements: When a company makes improvements or modifications to leased property or facilities, these enhancements become fixed assets.

- Computer Software: Purchased or developed software for business purposes is considered a fixed asset. It falls under the category of intangible assets if it is not physically tangible.

Each type of fixed asset brings unique value to a company’s operations and contributes to its long-term growth and success. Proper management and strategic utilization of these assets are vital for maximizing their potential and optimizing overall business performance.

What are the characteristics of fixed assets?

Fixed assets possess several key characteristics that distinguish them from other types of assets. These characteristics include:

- Long-Term Use: Fixed assets are acquired to use them for an extended period, typically exceeding one year. They are not meant for immediate resale or consumption but are crucial to the company’s long-term operations.

- Physical Existence: Unlike intangible assets, fixed assets have a tangible and visible form. They can be seen, touched, and physically identified. For example, buildings, machinery, vehicles, and land are tangible fixed assets.

- Cost: Fixed assets generally involve substantial initial costs or investments for acquisition, installation, and setup. These assets represent a considerable financial commitment for the company and are expected to provide value over their useful life.

- Value Generation: Fixed assets are expected to generate value or revenue for the company during their useful life. For instance, a manufacturing company’s machinery helps produce goods that are sold, contributing to revenue generation.

- Depreciation: Over time, fixed assets experience wear and tear, technological obsolescence, or other factors that reduce their value. Companies apply depreciation to account for this decline in value, spreading the asset’s cost over its useful life on the balance sheet and income statement.

- Use in Business Operations: Fixed assets are used in the company’s day-to-day operations to support its core business activities. Whether manufacturing products, providing services, or operating a facility, fixed assets facilitate these operations.

- Ownership and Control: Fixed assets are owned and controlled by the company. They are not held for sale as inventory or traded as financial instruments but form part of the company’s long-term asset base.

Understanding these characteristics is vital for proper accounting, management, and strategic decision-making related to fixed assets. Companies need to keep accurate records, assess the assets’ useful life, and plan for maintenance and upgrades to maximize their value and support business growth effectively.

What are the examples of fixed assets?

Examples of fixed assets encompass a wide range of tangible and intangible assets that businesses utilize for their operations and long-term value creation.

Here are some common examples:

- Buildings: Commercial properties, office buildings, warehouses, and manufacturing facilities owned by the company for its operations.

- Machinery and Equipment: Production machinery, assembly lines, computers, servers, vehicles, and tools used to manufacture goods or provide services.

- Land: Land owned for business purposes, such as for construction, expansion, or future development.

- Furniture and Fixtures: Office furniture, desks, chairs, cabinets, and fixtures used in retail or hospitality environments.

- Intangible Assets: Though not physically tangible, certain assets hold significant value. Examples include patents (rights to inventions or innovations), trademarks (distinctive signs representing a brand), copyrights (protection for original creative works), and software licenses.

- Investments in Subsidiaries: Ownership stakes in other companies that the business intends to hold for the long term.

- Leasehold Improvements: Improvements or alterations made to leased property to enhance its functionality and meet specific business needs.

- Natural Resources: Assets such as oil reserves, mineral deposits, timberland, or water rights that have economic value and a limited life span.

- Goodwill: The value of a company’s reputation, customer base, and brand loyalty, often arising from successful business operations and customer satisfaction.

- Long-Term Financial Investments: Long-term investments in financial instruments, such as long-term bonds or other securities.

These examples demonstrate the diversity of fixed assets and their vital role in supporting various industries and business operations. Proper management and optimization of these assets are essential for businesses to thrive and succeed in their respective markets.

Suggested Read: Capital Budgeting: What is it, Types, Methods, Process & Examples

Accounting for fixed assets

Accounting for fixed assets involves a series of processes to record their acquisition, depreciation, and eventual disposal accurately. The primary steps in accounting for fixed assets are as follows:

- Initial Recognition: When a company acquires a fixed asset, it must be recorded in the accounting books. The asset’s cost, including all directly attributable expenses (e.g., shipping, installation, legal fees), is capitalized as the initial cost of the asset.

- Depreciation: Fixed assets are subject to depreciation, reflecting their gradual loss of value over time due to wear and tear, obsolescence, or other factors. Companies choose a depreciation method (e.g., straight-line, declining balance) and estimate the asset’s useful life to allocate its cost over that period.

- Recording Depreciation Expense: Each accounting period, a portion of the fixed asset’s cost is recorded as depreciation expense on the income statement. This allocation helps match the asset’s cost with the revenue it generates, as required by the matching principle in accounting.

- Accumulated Depreciation: The total depreciation charged on a fixed asset is accumulated in a separate account called “Accumulated Depreciation.” This account is a contra-asset account and reduces the asset’s carrying value on the balance sheet.

- Asset Impairment: If a fixed asset’s value declines significantly, either due to external factors or impairment indicators within the company, an impairment loss may be recognized to adjust the asset’s carrying value to its recoverable amount.

- Disposal: When a fixed asset is sold, scrapped, or otherwise disposed of, the company records the transaction. The asset’s cost and accumulated depreciation are removed from the books, and any gain or loss on the disposal is recognized on the income statement.

- Revaluation: Some companies may choose to revalue their fixed assets periodically to reflect changes in fair market value. Revaluation adjusts the asset’s carrying value and accumulated depreciation to the revalued amount.

Fixed assets on financial statements

Fixed assets are prominently featured on a company’s financial statements, providing essential information about the company’s asset base and its long-term investments. The primary financial statements where fixed assets are presented include the balance sheet and related notes:

1. Balance Sheet

Fixed assets are listed on the balance sheet under the category of non-current assets, also known as long-term assets. These assets are not expected to be converted into cash or used up within one year. Fixed assets are typically presented in descending order of liquidity, with the most liquid non-current assets shown first.

- On the asset side of the balance sheet, fixed assets are reported at their historical cost, including all costs directly attributable to bringing the asset to its working condition for its intended use.

- The cumulative depreciation charged on fixed assets is shown as a negative value in a contra-asset account called “Accumulated Depreciation.” This amount reduces the fixed assets’ carrying value to arrive at their net book value or net carrying amount.

2. Notes to Financial Statements

The notes to the financial statements provide additional information about fixed assets. This may include details on the depreciation method used, the estimated useful lives of the assets, any significant impairment losses recognized, and any changes in accounting policies related to fixed assets.

The presentation of fixed assets on the balance sheet helps stakeholders, including investors, creditors, and analysts, understand the company’s asset composition, its investment in productive resources, and how these assets contribute to the company’s financial position.

Importance of proper fixed asset management

Proper fixed asset management is of utmost importance for businesses and organizations for several compelling reasons. Firstly, it ensures optimized asset utilization, allowing companies to make the most of their investments and resources. By maximizing the productivity and efficiency of fixed assets, businesses can reduce operational costs and improve overall profitability.

Secondly, effective fixed asset management ensures accurate and reliable financial reporting. By maintaining accurate records of fixed assets, including their initial costs, depreciation, and disposal, companies can present a clear and transparent picture of their financial health on their balance sheets and income statements. This, in turn, enhances credibility and fosters trust among investors, creditors, and stakeholders.

Thirdly, proper asset management enables compliance with accounting standards, tax regulations, and legal requirements. By adhering to these guidelines, businesses can avoid potential penalties, fines, or legal liabilities, safeguarding their reputation and financial stability.

Moreover, strategic decision-making heavily relies on the condition and lifecycle of fixed assets. By having a comprehensive understanding of asset performance and depreciation, companies can make informed choices regarding maintenance, upgrades, or replacements. This empowers them to align their investment strategies with their long-term business goals, staying competitive and adaptable in a dynamic market environment.

Benefits of effective fixed asset management

Effective fixed asset management offers numerous benefits to businesses and organizations, contributing to their overall success and financial well-being. Some key benefits include:

- Optimized Asset Utilization: Proper asset management ensures that fixed assets are used efficiently, reducing downtime and maximizing their productivity. This leads to cost savings and improved operational efficiency.

- Accurate Financial Reporting: Effective asset management enables accurate and up-to-date financial reporting. Companies can present a clear and transparent picture of their asset base, depreciation, and overall financial health to stakeholders, instilling confidence and trust.

- Compliance and Risk Mitigation: Adhering to proper asset management practices ensures compliance with accounting standards, tax regulations, and legal requirements. It mitigates the risk of financial penalties, legal issues, or reputational damage due to non-compliance.

- Informed Decision-making: Detailed records of fixed assets empower businesses to make informed strategic decisions. Companies can identify underperforming assets, plan for replacements or upgrades, and align investments with their long-term objectives.

- Cost Control and Budgeting: Effective asset management helps identify unnecessary assets and reduces overspending on new acquisitions. It aids in allocating budgets efficiently, optimizing resource utilization.

- Enhanced Productivity and Competitiveness: Well-managed fixed assets contribute to improved overall productivity, giving businesses a competitive edge. Efficient asset use leads to better production output, faster delivery times, and superior customer service.

- Asset Tracking and Loss Prevention: Proper tracking and documentation prevent asset misplacement or theft. This protects the company’s investment and reduces the financial impact of lost assets.

- Sustainable Practices: Effective asset management promotes sustainability by optimizing asset use, reducing waste, and making environmentally conscious decisions during asset lifecycle management.

Also, Read: 10 Best Business Budgeting Software & Tools

Risks of inadequate fixed asset management

Inadequate fixed asset management poses several risks to businesses and organizations, which can have significant negative impacts on their operations and financial health. Some of the key risks include:

- Financial Reporting Errors: Inadequate management of fixed assets can result in errors in financial reporting. Incorrectly recorded or depreciated assets can distort the company’s financial statements, leading to inaccurate portrayals of its financial position and performance.

- Non-compliance and Legal Issues: Failing to adhere to accounting standards, tax regulations, or legal requirements regarding fixed assets can expose the company to compliance issues and potential legal consequences, such as penalties, fines, or audits.

- Asset Underutilization: Poor asset management may lead to underutilization of fixed assets. This means that valuable resources are not being used to their full potential, resulting in reduced productivity and efficiency.

- Increased Maintenance Costs: Neglected or poorly maintained assets may lead to higher maintenance costs in the long run. Regular maintenance is essential to prevent breakdowns and extend the useful life of assets.

- Lost Revenue Opportunities: Inadequate fixed asset management can result in missed revenue opportunities. Underperforming assets or inefficiencies in asset usage can impact the company’s ability to meet customer demands or seize business opportunities.

- Asset Misplacement or Theft: Without proper tracking and documentation, fixed assets can be misplaced, lost, or subject to theft. This can lead to financial losses and disrupt business operations.

- Inefficient Resource Allocation: Inadequate asset management hinders effective resource allocation. Companies may overspend on unnecessary assets or delay crucial replacements or upgrades, affecting overall business performance.

- Negative Impact on Business Reputation: Poorly managed fixed assets can reflect poorly on the company’s reputation and credibility. This may affect relationships with investors, customers, and business partners.

Fixed asset Vs Current asset

Aspect |

Fixed Assets |

Current Assets |

| Definition | Tangible or intangible assets | Assets expected to be converted into cash or used up within one year or operating cycle of the business |

| Purpose | Used for long-term business operations | Used for short-term operational needs |

| Nature | Physical or intangible | Primarily financial or cash-based |

| Holding Period | Held for more than one year | Held for less than one year |

| Liquidity | Less liquid | More liquid |

| Examples | Land, buildings, machinery, patents, trademarks | Cash, accounts receivable, inventory, short-term investments |

| Valuation on Balance Sheet | Reported at historical cost less accumulated depreciation | Reported at the lower of cost or market value (Net Realizable Value) |

| Depreciation | Subject to depreciation over their useful life | Not subject to depreciation |

| Role in Financial Statements | Reported under non-current assets on the balance sheet | Reported under current assets on the balance sheet |

| Risk and Return | Generally, fixed assets offer higher returns with associated risks | Current assets offer lower returns with lower associated risks |

| Management Focus | Focus on long-term value and strategic planning | Focus on day-to-day operations and short-term cash flow management |

Fixed assets tracking and documentation

Fixed assets tracking and documentation involve a systematic process to monitor and record relevant information about each fixed asset throughout its lifecycle. The key steps in tracking and documentation are as follows:

- Asset Identification: Assign a unique identifier or tag to each fixed asset to differentiate it from others. This identifier can be a barcode, QR code, or asset number, making it easier to track and locate the asset.

- Asset Registration: Create a detailed record for each fixed asset, capturing essential information such as the asset’s description, acquisition date, cost, useful life, location, and any warranty or maintenance details.

- Physical Verification: Conduct periodic physical verification of fixed assets to ensure that the records accurately reflect their actual presence and condition. This helps identify missing, lost, or stolen assets and ensures the accuracy of asset data.

- Maintenance Records: Maintain a log of all maintenance activities performed on each fixed asset. This includes routine maintenance, repairs, upgrades, and any associated costs.

- Depreciation Tracking: Track the depreciation of fixed assets over time. Keep a record of the depreciation method used, the estimated useful life, and the accumulated depreciation for each asset.

- Asset Movements: Record any transfers or movements of fixed assets between different departments, locations, or projects. This ensures that the asset’s current location and custodian are always up-to-date.

- Disposal Documentation: Document the disposal or retirement of fixed assets. Record the reason for disposal, the date, method of disposal (sale, scrapping, donation), and any gains or losses incurred.

- Digital Asset Management Systems: Utilize digital asset management systems or fixed asset tracking software to streamline the process. These systems provide centralized databases, barcode scanning capabilities, and reporting functionalities for efficient asset management.

- Auditing and Compliance: Regularly conduct internal audits to review the accuracy and completeness of fixed asset records. Ensure compliance with accounting standards, tax regulations, and company policies.

Fixed assets disposal and retirement

1. Reasons for Disposal

Fixed assets may be disposed of for various reasons, including:

- Obsolescence: The asset has become outdated and no longer serves the company’s operational needs efficiently.

- End of Useful Life: The asset has reached the end of its estimated useful life and is no longer productive.

- Damage or Wear and Tear: The asset is extensively damaged or worn out, making it uneconomical to repair or continue using.

- Redundancy: Due to changes in business operations or technological advancements, the asset is no longer required.

- Upgrades or Replacements: The asset is being replaced by a newer, more efficient model or upgraded version.

- Financial Considerations: The company may need to raise funds, and selling the asset provides a source of cash.

2. Methods of Disposal

- Sale: The fixed asset is sold to a third party in exchange for cash or other assets. The company recognizes a gain or loss on the disposal, depending on whether the sale proceeds exceed or are less than the asset’s carrying amount (cost minus accumulated depreciation).

- Donation: The company may choose to donate the fixed asset to a charitable organization or a non-profit entity. In this case, the company recognizes a gain or loss on the donation based on the asset’s fair market value at the time of donation.

- Scrapping: If the asset has no residual value or is in poor condition, it may be scrapped, and no proceeds are received. The company records a loss on the disposal, considering the difference between the asset’s carrying amount and the proceeds received from scrapping, if any.

3. Retirement of Fixed Assets

Retirement of fixed assets occurs when an asset is removed from service without any proceeds received, typically due to complete obsolescence or impairment. The asset’s cost and accumulated depreciation are removed from the books, resulting in a loss on retirement.

4. Accounting Treatment of Disposal and Retirement

When disposing of a fixed asset, the accounting treatment involves:

- Removing the asset’s cost from the balance sheet.

- Removing the accumulated depreciation from the accumulated depreciation account.

- Recognizing any gain or loss on disposal in the income statement.

For retirement, the accounting treatment is similar

- Remove the asset’s cost from the balance sheet.

- Remove the accumulated depreciation from the accumulated depreciation account.

- Recognize any loss on retirement in the income statement.

Proper accounting treatment ensures that the company’s financial statements accurately reflect the removal of fixed assets from its books and appropriately account for any gains or losses associated with the disposal or retirement.

Tax implication for fixed assets

1. Tax Implications of Fixed Assets

Fixed assets have significant tax implications for businesses, as they impact taxable income, deductions, and overall tax liabilities. Some key tax implications of fixed assets include:

- Depreciation Deduction: Businesses can claim depreciation deductions for fixed assets over their useful life in many tax jurisdictions. This allows the company to deduct a portion of the asset’s cost from its taxable income each year, reducing the tax burden.

- Capital Expenditure vs. Revenue Expenditure: Tax regulations differentiate between capital expenditures (investments in fixed assets) and revenue expenditures (operational expenses). Capital expenditures are generally not fully deductible in the purchase year but depreciate over time. Revenue expenditures, on the other hand, are fully deductible in the year they are incurred.

- Capital Gains and Losses: The sale of fixed assets may result in capital gains or losses, depending on whether the selling price exceeds or is less than the asset’s adjusted cost basis. Capital gains are typically taxed, while capital losses may be used to offset capital gains or carried forward to future tax years.

- Tax Credits and Incentives: Some jurisdictions offer tax credits or incentives for certain types of fixed assets, such as energy-efficient equipment or investments in specific industries. Taking advantage of these credits can reduce the company’s overall tax liability.

- Section 179 Deduction (U.S.): In the United States, the Section 179 deduction allows small businesses to deduct the full cost of qualifying fixed assets in the year of purchase rather than depreciating them over time. This provides immediate tax benefits for eligible asset investments.

2. Capital Allowances and Depreciation for Tax Purposes

Capital allowances and depreciation are methods used in different countries to calculate the tax deduction for fixed assets. While the concept is similar, the terminology may vary.

- Capital Allowances (UK and some other countries): Capital allowances are tax deductions claimed on qualifying capital expenditures, including fixed assets. The tax legislation of each country specifies the rates and rules for claiming capital allowances, allowing businesses to deduct a portion of the asset’s cost from their taxable income over time.

- Depreciation (U.S. and some other countries): Depreciation is the systematic allocation of the cost of fixed assets over their estimated useful life for tax purposes. The U.S. tax code, for example, provides depreciation schedules for various asset classes, allowing businesses to deduct the appropriate depreciation expense annually.

Both capital allowances and depreciation aim to provide tax benefits for businesses investing in fixed assets while recognizing the reduction in value over time. They play a crucial role in determining the taxable income and overall tax liabilities for businesses and are essential considerations in tax planning and financial decision-making.

Must Read: CapEx vs. OpEx: A Guide to Understanding the Differences

Fixed assets in the context of IFRS and GAAP

1. International Financial Reporting Standards (IFRS)

IFRS is a set of accounting standards developed by the International Accounting Standards Board (IASB) to provide a common global framework for financial reporting. It is widely used in many countries and by large multinational corporations. IFRS ensures transparency, comparability, and consistency in financial reporting across different jurisdictions.

2. Generally Accepted Accounting Principles (GAAP)

GAAP refers to the accounting principles, standards, and procedures used in the United States. It is established by the Financial Accounting Standards Board (FASB) and is the standard framework for financial reporting in the U.S. GAAP principles that aim to provide accurate and relevant information to investors, creditors, and other stakeholders.

3. Key Differences in Fixed Asset Accounting

While both IFRS and GAAP share similarities in fixed asset accounting, some key differences exist:

- Valuation of Fixed Assets: Under IFRS, fixed assets are initially measured at historical cost but can be revalued to fair value in certain circumstances. In contrast, GAAP generally requires fixed assets to be recorded at historical cost and prohibits the use of revaluation.

- Depreciation Methods: IFRS allows a variety of depreciation methods, such as straight-line, reducing balance, and units of production, based on the consumption pattern. GAAP, on the other hand, generally requires the straight-line method for financial reporting purposes.

- Impairment Testing: IFRS requires regular impairment testing of fixed assets whenever there is an indication of impairment. If the carrying amount exceeds the recoverable amount, the asset must be written down to its recoverable amount. GAAP follows a two-step impairment model, where the asset is written down to fair value if it is impaired.

- Componentization: IFRS encourages componentization, where significant components of a fixed asset with different useful lives are depreciated separately. GAAP does not mandate componentization and typically depreciates the entire asset as a single unit.

- Disclosure Requirements: IFRS tends to have more extensive disclosure requirements for fixed assets compared to GAAP, especially related to revaluations, impairment testing, and changes in accounting policies.

- Lease Accounting: IFRS 16 introduces significant changes to lease accounting, bringing operating leases onto the balance sheet. In contrast, GAAP has historically distinguished between operating and capital leases, with only capital leases recognized on the balance sheet.

As accounting standards continuously evolve and converge, the differences between IFRS and GAAP may decrease over time. However, it is crucial for companies operating in multiple jurisdictions to be aware of these variations and comply with the appropriate accounting standards for their financial reporting.

Managing fixed assets throughout their life cycle

- Planning and Budgeting for New Fixed Assets: Involves identifying the need for new fixed assets, assessing their cost and benefits, and incorporating them into the company’s budget. Proper planning ensures that new assets align with business goals and are financially feasible.

- Regular Maintenance and Repairs: Involves implementing scheduled maintenance routines and timely repairs to keep fixed assets in optimal working condition. Regular maintenance extends the asset’s useful life and reduces the risk of breakdowns, minimizing downtime and repair costs.

- Renewal and Upgrading Strategies: Involves evaluating fixed assets periodically to determine if renewal or upgrading is necessary. This may involve replacing obsolete assets with newer, more efficient models or upgrading existing assets to meet evolving business needs. Renewal and upgrading strategies ensure that fixed assets remain relevant and contribute to operational efficiency.

Read More: 10 Best Asset Management Software Systems

Fixed Assets Software Solutions

Benefits of Fixed Asset Management Software

Fixed asset management software offers numerous advantages, including:

- Improved Accuracy and Efficiency: Automating asset tracking and documentation reduces human errors and streamlines processes, leading to more accurate and efficient asset management.

- Real-time Visibility: Software solutions provide real-time visibility into asset data, enabling businesses to make informed decisions and optimize asset utilization.

- Compliance and Reporting: Fixed asset software helps ensure compliance with accounting standards and tax regulations, simplifying financial reporting and audits.

- Cost Savings: Effective asset management reduces maintenance and repair costs, extends asset life, and prevents losses from misplaced or underutilized assets.

- Centralized Database: Software centralizes asset information, making it easily accessible to authorized personnel, enhancing collaboration, and eliminating data silos.

- Depreciation Management: Automated depreciation calculations ensure accurate and consistent recording of asset depreciation over time.

Features to Look for in a Fixed Asset Software

When choosing fixed asset management software, consider the following essential features:

- Asset Tracking: Robust asset tracking capabilities with unique identifiers, barcode scanning, or GPS integration for accurate and real-time asset location.

- Depreciation Methods: Support for various depreciation methods to cater to different accounting standards and business needs.

- Maintenance Scheduling: Built-in maintenance schedules and reminders to ensure timely upkeep of assets.

- Reporting and Analytics: Customizable reports and analytics to gain insights into asset performance and financial data.

- Integration Capabilities: Compatibility with other business systems like accounting software, ERP, or CMMS for seamless data transfer.

- User Access Control: Role-based access control to restrict access to sensitive asset information.

Popular Fixed Asset Management Software Options

Some popular fixed asset management software options include:

- IBM Maximo: A comprehensive asset management solution that offers asset tracking, maintenance planning, and regulatory compliance features.

- SAP Asset Accounting: Part of the SAP ERP suite, it provides robust asset tracking and accounting functionalities.

- Oracle Fixed Assets: An integrated module in the Oracle E-Business Suite for managing fixed assets, depreciation, and tax compliance.

Future Trends in Fixed Asset Management

- Integration of IoT and AI in Asset Tracking: Internet of Things (IoT) sensors and Artificial Intelligence (AI) will play a significant role in asset tracking. IoT devices can provide real-time data on asset location, condition, and performance, while AI algorithms can analyze this data to optimize asset utilization and predict maintenance needs.

- Sustainability and Green Asset Management: With growing environmental awareness, businesses will focus on sustainable asset management practices. Green asset management involves tracking and optimizing assets’ environmental impact, promoting energy-efficient assets, and considering the asset’s end-of-life disposal with minimal environmental impact.

- Evolving Regulations and Their Impact on Fixed Asset Accounting: Changing accounting standards and regulations will continue to influence fixed asset accounting practices. Companies must adapt to evolving requirements and ensure compliance with international and local accounting standards, which could impact how assets are valued, depreciated, and reported on financial statements.

FAQs

The number of fixed assets varies for each company and depends on the size and nature of the business.

In Tally, fixed assets refer to assets like land, buildings, machinery, etc., used for long-term business operations and not meant for sale.

Non-fixed assets, also known as current assets, are assets that are expected to be converted into cash or used up within one year or the operating cycle of the business.

The advantages of fixed assets include long-term utility, capital appreciation, production efficiency, and potential tax benefits through depreciation deductions.

Fixed assets in the balance sheet represent the total value of long-term tangible and intangible assets owned by the company.

The worth of fixed assets is determined by their historical cost, less accumulated depreciation or impairment.

Fixed assets in a company typically include land, buildings, machinery, vehicles, equipment, furniture, patents, and trademarks.

Fixed assets impact the company’s financial statements through their initial recognition, depreciation, impairment, and disposal, which affect the balance sheet, income statement, and cash flow statement.

Fixed assets are initially recorded at cost and subsequently depreciated or amortized over their useful lives. They are valued on the balance sheet at historical cost, net of depreciation or impairment.

Depreciation is systematically allocating a fixed asset’s cost over its estimated useful life. It is an accounting method used to recognize the wear and tear of assets over time.

While most fixed assets depreciate in value over time due to wear and tear, some assets like land and certain intellectual property can appreciate in value.

Yes, companies can lease or rent fixed assets instead of purchasing them outright, which provides flexibility and may have tax advantages.

Companies consider factors like maintenance costs, asset condition, technological advancements, and the impact on productivity and safety to determine whether to repair or replace fixed assets.

Fixed assets can serve as collateral for loans or financing, providing lenders with security in case of default.

Yes, specific accounting standards, such as IFRS and GAAP, provide guidelines for recognizing, measuring, and disclosing fixed assets.

Businesses can maximize the value and efficiency of fixed assets through effective asset management, regular maintenance, upgrades, and optimization of asset utilization.

Efficient fixed asset management can positively impact a company’s profitability by reducing costs, improving productivity, and prolonging the useful life of assets.

Companies handle fixed asset impairment by conducting regular impairment tests and recognizing impairment losses when the carrying amount exceeds the recoverable amount.